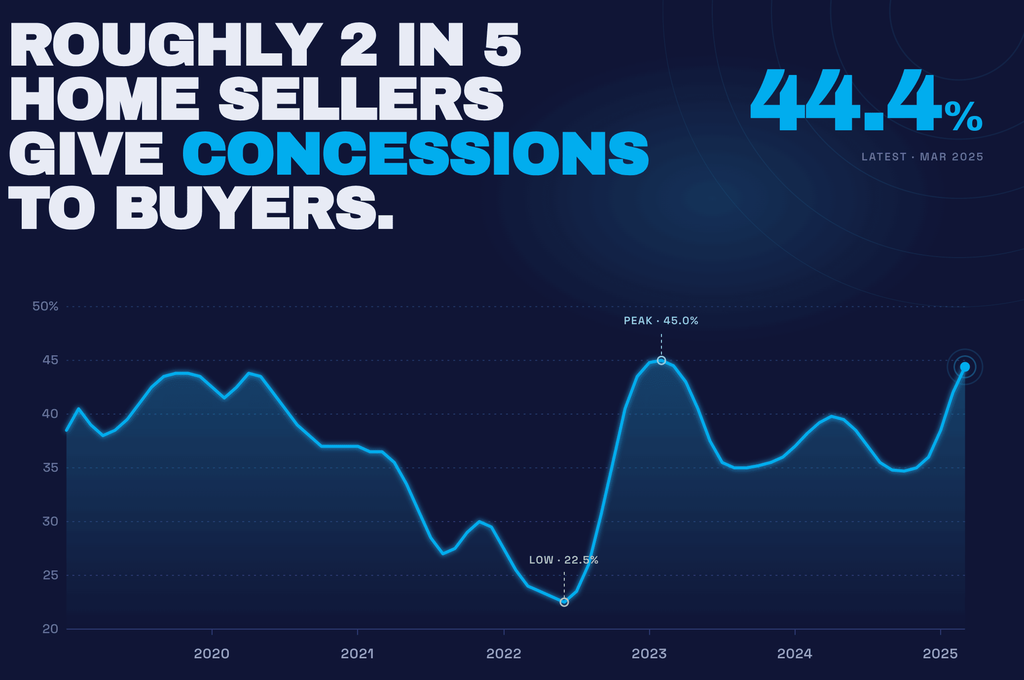

Nationally, roughly two in five home sellers gave concessions to buyers in the first quarter of 2025. That number, tracked by Redfin, is near the highest it has been in years, close to the 2023 peak of 45 percent, and well above the 22.5 percent low hit during the frenzied seller’s market of 2022.

Source: Redfin. Roughly 2 in 5 home sellers gave concessions to buyers as of March 2025. The national rate hit a low of 22.5% during the 2022 seller’s market and has climbed back near the 2023 peak of 45%.

That statistic matters as context, but it describes a national market that looks very different from what is happening in Reston. If you are a Reston homeowner preparing to sell, or already under contract and navigating a concession request, the national number is a starting point, not a playbook.

Here is what the local data actually shows, what the four main types of concessions are, and how to think through each one in the context of this specific market.

Why Reston’s Market Holds Differently Than Most

Reston is not a generic suburb. The economic foundation here is genuinely different from most of the country, and that matters a lot when you are thinking about how much leverage you have as a seller.

The area sits inside one of the most concentrated corridors of federal government employment in the country. Agencies, contractors, and tech firms tied to defense and intelligence, including SAIC, Leidos, General Dynamics IT, and Booz Allen Hamilton, employ tens of thousands of people within a short commute of Reston. That workforce tends to be highly educated, well compensated, and relatively insulated from the economic swings that push concession rates higher in other parts of the country.

The Silver Line extension brought two Metro stations directly into Reston: Reston Town Center and Wiehle-Reston East. For buyers who commute into Washington, D.C., that access commands a premium that simply does not exist in markets without it. The combination of walkable amenities at Reston Town Center, trail access through the Washington and Old Dominion Trail, and the general livability of the area creates sustained demand that does not evaporate when interest rates rise.

Fairfax County schools, consistently rated among the strongest in Virginia, add another layer of demand that tends to keep the buyer pool engaged even when the broader market softens. Buyers with school-age children do not casually pass on a market like this.

None of that means sellers have unlimited leverage. It means the baseline here is higher than most places, and that context shapes how concession conversations should go.

What the March 2026 Numbers Show

The most recent data for Reston covers March 2026, and it tells a nuanced story.

On the demand side, the market is genuinely active. Closed sales came in at 94 units, up nearly 19 percent from March 2025. New pendings hit 114, up 3.6 percent year over year. Dollar volume for the month was $65.8 million, an 18.4 percent increase from the same period last year. These are not the numbers of a market in distress.

The average sold-to-original-list-price ratio held at 100.7 percent. Sellers in Reston were still, on average, receiving more than their asking price. Detached homes showed even stronger dynamics, averaging 103.6 percent of original list price with an average days on market of just 12 days. The median sold price for detached homes in March was $1,225,250, up 12.4 percent from March 2025.

The attached and townhouse segment tells a slightly different story. Average days on market for those sales ran 28 days in March, up significantly from 13 days in the prior year period. The median sold price for attached homes held at $710,000, essentially flat year over year. Supply in the attached segment has grown, and buyer selection has increased.

The broader headline for all home types shows days on market jumping from 11 to 21 days year over year, nearly doubling. More listings are sitting longer than they were a year ago, and the median sold price across all types came in at $600,000, down from $685,000 in March 2025. That shift in the median is partly compositional, as more attached sales were in the mix, but it reflects a real change in the pace of negotiation.

So the honest picture is this: detached homes in Reston are still moving with strength, and buyers are competing for them. Attached homes and condos are in a more patient market where concession conversations are more likely to arise. Sellers who understand which segment they are in, and what the friction actually is for their specific buyer, will navigate these conversations much better than those who treat every concession request the same way.

The Four Types of Concessions, and What Each One Actually Does

Concessions is a word that covers very different tools. Treating them interchangeably is where most sellers get into trouble. Here is a breakdown of the four most common types and when each one makes sense.

1. Closing-Cost Credit

A closing-cost credit is a dollar amount the seller agrees to contribute toward the buyer’s closing costs at settlement. It shows up as a seller credit on the settlement statement.

In Northern Virginia, buyers typically face $10,000 to $18,000 in closing costs on a $600,000 to $750,000 purchase. These costs include lender origination fees, title insurance, transfer taxes, and prepaid escrow items. For a buyer who is fully qualified on income and credit but stretched thin at the closing table, a $10,000 credit can be the difference between executing on a home they genuinely want and walking away.

The important structural detail: closing-cost credits are subject to loan limits. Most loan programs cap seller concessions as a percentage of the purchase price, typically 3 to 6 percent depending on the loan type and down payment. A credit also cannot artificially inflate a purchase price above appraised value, so there is a ceiling to how much can flow through this mechanism. Your agent should run the specific numbers based on your buyer’s financing before agreeing to any amount.

When this works in Reston: A well-qualified buyer is purchasing an attached home or condo in the $450,000 to $650,000 range. The home is priced correctly, the buyer genuinely wants it, but their reserve position post-closing is the actual obstacle. A targeted credit solves a real problem and keeps the deal moving.

When it does not work: The listing is overpriced, buyer interest is weak, and a closing-cost credit is being offered as a way to generate showings. A credit does not solve a pricing problem. Buyers who are not already close will not be pulled in by a credit.

2. Repair Credit

A repair credit replaces the requirement for the seller to complete repairs before closing. Instead of getting work done, the seller offers a dollar amount that the buyer uses post-closing to address inspection items.

In a market like Reston, where older townhomes and condos in communities like Hunters Woods, Shadowood, and Lakewinds are common, inspection findings are almost a given. HVAC systems age, roofs wear, water intrusion issues appear in older attached construction. The question is not whether something will come up. It is how to handle it efficiently when it does.

A repair credit has a real advantage over required repairs: speed. Repairs take time, require coordinating contractors, and introduce risk. A repair completed hastily before closing may raise more questions than it resolves. A credit agreed upon quickly keeps the timeline intact and gives the buyer control over who does the work.

The practical challenge is arriving at the right number. Buyers and sellers frequently disagree on repair costs because neither party has a firm contractor estimate in hand. Experienced agents will frame this conversation around a reasonable range, not a single figure, and often suggest the parties split the difference rather than fight over a number that is inherently uncertain.

When this works in Reston: Inspection surfaces a known issue, such as a roof at the end of its life, an HVAC system from 2008, or a water heater past its service window. Both parties want to close. A credit for a reasonable amount keeps the deal together without the delay and risk of contractor scheduling.

When it does not work: Inspection reveals systemic issues, including foundation concerns, major structural problems, or significant undisclosed water damage. In those situations, a credit is not a substitute for the seller addressing the root cause or for a meaningful price adjustment.

3. Rate Buydown

A rate buydown uses seller funds to reduce the buyer’s interest rate, either temporarily or permanently.

A permanent buydown involves paying discount points at closing to lower the rate for the life of the loan. A temporary buydown reduces the rate for the first one to three years before stepping up to the note rate. The 2-1 buydown, where the rate is 2 percent below the note rate in year one and 1 percent below in year two, became a frequently used tool when rates climbed and buyers felt the payment pressure acutely.

These two structures serve different buyers. A permanent buydown makes sense for a buyer planning to stay long-term who wants every payment lower. A temporary buydown appeals to a buyer who expects to refinance within a few years, or whose income is growing and who just needs year-one and year-two payment relief to feel comfortable committing.

On the seller’s side, a buydown costs real money upfront. On a $700,000 loan, a 2-1 buydown might run $10,000 to $14,000 in seller-funded points. For a buyer who is otherwise qualified but sitting on the fence because of payment sensitivity, that cost can be worth absorbing if it gets the deal done and protects the list price from a reduction.

When this works in Reston: A detached home is priced appropriately and has good buyer interest, but monthly payment concerns are the specific obstacle. The buyer likes the house and the neighborhood but is not fully committed because the payment at current rates strains their budget. A buydown closes that gap.

When it does not work: The home has a fundamental pricing or condition problem. A lower rate does not make buyers overlook a house that needs $80,000 in deferred maintenance or that is priced well above where the market is actually valuing it.

4. Prepaid-Item Help

Prepaids are the line items at closing that fund the escrow account and cover costs due immediately: homeowners insurance (often a full year paid upfront), property tax escrow deposits, and per-diem interest from the closing date to the end of the month.

In Fairfax County, property tax escrow requirements alone can run $4,000 to $7,000 at closing on a typical Reston purchase, depending on assessed value and timing. Add a year of homeowners insurance and the per-diem interest, and a buyer who thought they had closing costs covered can find themselves short by $5,000 to $8,000 more than expected.

Prepaid-item help addresses that specific gap. It differs from a general closing-cost credit in that it is targeted at these funding items rather than lender fees or title costs, though in practice the credits often flow through the same settlement-statement mechanism.

When this works in Reston: A buyer is financially solid, has made it through underwriting, and is genuinely close to the finish line. Their closing costs are covered but the prepaid escrow setup created an unexpected shortfall. A targeted credit gets a ready buyer across the line.

When it does not work: The buyer is not yet fully qualified, or the shortfall is a symptom of a larger cash problem. Prepaid-item help works on the margins, not on fundamentally undercapitalized buyers.

Concessions vs. Price Cuts: The Distinction That Actually Matters

A price cut changes the public story about your home. It signals to every buyer who has seen the listing, and to anyone who pulls it up later, that the seller moved. In a market like Reston where comparable sales matter for appraisals, price cuts also affect the neighborhood’s pricing record.

A concession changes the closing structure, not the headline. The list price holds. The sold price holds. The credit flows through the settlement statement without appearing in the public pricing history in the same way.

That distinction is not always decisive. If a listing is overpriced and buyers are not interested, a concession offers nothing. The problem is market-credibility friction, and the only tool that solves that is a price correction. Credits and buydowns cannot manufacture buyer interest.

But when a Reston home is priced well, showing consistently, and stalling at the offer stage because of financing structure or closing cost gaps, a targeted concession is almost always a better tool than a price cut. The seller protects the pricing story, the buyer gets the help they actually need, and the deal closes.

The sellers who navigate this best are the ones who understand, before any offer arrives, what kind of friction is most likely to come up for their specific home. That is a conversation worth having with your agent before you go live, not after a buyer asks.

What to Think Through Before Your Listing Goes Active

A concession only works when it is targeted at the actual problem. That sounds obvious, but in a negotiation it is easy to reach for the familiar tool rather than the right one.

Before your Reston home hits the market, it is worth working through a few specific questions. Who is the likely buyer for your home: a first-time buyer stretching on cash, a move-up buyer with equity but payment sensitivity, or an all-cash buyer to whom concessions are largely irrelevant? What does the inspection history look like for comparable homes in your community? What are rates doing, and is monthly payment sensitivity something your probable buyer will feel acutely?

None of this requires a crystal ball. It requires an agent who knows the local market well enough to anticipate where deals typically slow down for your type of home and your price range, and to have a clear framework ready before you need it.

Reston’s market is strong enough that many sellers will not face concession requests at all, particularly in the detached segment. But the attached and condo market has lengthened, buyer selection has increased, and having a clear-eyed framework before you get an offer is almost always better than improvising under pressure once one arrives.

If you are thinking about listing and want to talk through what is realistic for your specific home, reach out directly. These conversations are always easier before you are under contract than after.

Graham and Kathy Tracey are Reston and Herndon real estate agents with Compass. All market statistics referenced are from Bright MLS data for Reston, VA through March 2026, compiled by ShowingTime.